# We start with specifying our base image. Use the FROM keyword to do that -

# FROM tensorflow/tensorflow:2.3.0-gpu

# FROM tensorflow/tensorflow:latest-gpu

FROM tensorflow/tensorflow:nightly-gpu

RUN apt-get install -y locales

RUN sed -i -e 's/# en_US.UTF-8 UTF-8/en_US.UTF-8 UTF-8/' /etc/locale.gen && locale-gen

ENV LANG en_US.UTF-8

ENV LANGUAGE en_US:en

ENV LC_ALL en_US.UTF-8

# First, we set a working directory and then copy all the files for our app.

WORKDIR /usr/src/app

# copy all the files to the container

# adds files from your Docker client’s current directory.

COPY . .

RUN python3 -m pip install --upgrade pip

# install dependencies

# RUN pip install -r requirements.txt

RUN pip install numpy pandas sklearn matplotlib pandas_gbq

RUN apt-get install -y nano

RUN DEBIAN_FRONTEND="noninteractive" apt-get -y install tzdata

RUN ln -fs /usr/share/zoneinfo/Asia/Singapore /etc/localtime

RUN dpkg-reconfigure -f noninteractive tzdata

For cases where you will need to share directories between the host and the Docker, use:

docker run --name=docker_instance_name --gpus all -d -v ....

-v --volume=[host-src:]container-dest[:<options>]: Bind mount a volume.

-d to start a container in detached mode

--gpus GPU devices to add to the container (‘all’ to pass all GPUs)

Judea Pearl, a pioneering figure in artificial intelligence, argues that AI has been stuck in a decades-long rut. His prescription for progress? Teach machines to understand the question why.

All the impressive achievements of deep learning amount to just curve fitting

Now, Bengio says deep learning needs to be fixed. He believes it won’t realize its full potential, and won’t deliver a true AI revolution, until it can go beyond pattern recognition and learn more about cause and effect. In other words, he says, deep learning needs to start asking why things happen.

When we look at observational metrics, our Machine Learning models are doing great predicting a certain outcome given a treatment, but they are good exactly at that and not at the counterfactual – what would have been the outcome given no treatment

Hernán MA, Robins JM (2020). Causal Inference: What If. Boca Raton: Chapman & Hall/CRC

The book is divided in three parts of increasing difficulty: Part I is about causal inference without models (i.e., nonparametric identification of causal effects), Part II is about causal inference with models (i.e., estimation of causal effects with parametric models), and Part III is about causal inference from complex longitudinal data (i.e., estimation of causal effects of time-varying treatments).

Here are the top four reasons of why I think it’s a great book:

Detailed introduction to the key concepts including many examples

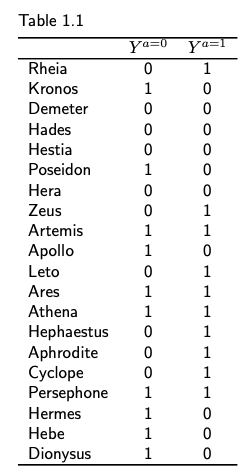

The first four chapters (a definition of causal effect, randomised experiments, observational studies and effect modification) cover key concepts such as potential outcomes (the outcome variable that would have been observed under a certain treatment value), individual and average causal effects, randomisation, identifiability conditions, exchangeability, positivity and consistency. You will get to know Zeus’s extended family, with many examples covering their various health conditions and treatment options. As an example, table 1.1 shows the counterfactual outcomes (die or not) under both treatment (a = 1 a heart transplant) and no treatment (a = 0). Providing practical examples along with the definition helps cement the learning by identifying the key attributes associated with the concept.

Practical approach

Starting from the introduction, the authors are quite clear about their goals

Importantly, this is not a philosophy book. We remain agnostic about metaphysical concepts like causality and cause. Rather, we focus on the identification and estimation of causal effects in populations, that is, numerical quantities that measure changes in the distribution of an outcome under different interventions. For example, we discuss how to estimate in patients with serious heart failure if they received a heart transplant versus if they did not receive a heart transplant. Our main goal is to help decision makers make better decisions

INTRODUCTION: TOWARDS LESS CASUAL CAUSAL INFERENCES

On top of it, the book comes with a large number of code example in both R and Python, covering the first two part including chapters 11-17. It would be great to see additional code examples covering part three (causal inference from complex longitudinal data).

You should start with reading the book, and on parallel fire-up

jupyter notebook

Jupiter notebook

and start playing with the code

A Python example (Chapter 17)

The validity of causal inferences models

The authors discuss a large number of non-parametric and parametric techniques and algorithms to calculate causal effects. But they keep reminding us that all of these techniques rely on untestable assumptions and on expert knowledge. As an example:

Unfortunately, no matter how many variables are included in L, there is no way to test that the assumption (conditional exchangeability) is correct, which makes causal inference from observational data a risky task. The validity of causal inferences requires that the investigators’ expert knowledge is correct

and

Causal inference generally requires expert knowledge and untestable assumptions about the causal network linking treatment, outcome, and other variables.

A (geeky) sense of humor

Technical books tend to be concise and dry, telling an anecdote or adding a joke can make difficult content more enjoyable and understandable.

As an example, when discussing the potential outcomes of the heart transplant treatment in Zeus’s extended family, here is how the authors introduced the issue of sampling variability:

At this point you could complain that our procedure to compute effect measures is somewhat implausible. Not only did we ignore the well known fact that the immortal Zeus cannot die, but more to the point – our population in Table 1.1 had only 20 individuals.

Chapter 1.4

As another example, chapter 7 introduces the topic of confounding variables using an observational study which is designed to answer the causal question “does one’s looking up to the sky make other pedestrians look up too?”. The plot develops and new details are being shared in chapters 8 (selection bias), chapter 9 (measurement bias) and chapter 10 (random variability), till the authors announce the following

Do not worry. No more chapter introductions around the effect of your looking up on other people’s looking up. We squeezed that example well beyond what seemed possible

Chapter 11

I hope that you will find this book useful and that you will enjoy learning about Causal Inference as much as I did!

I tensorflow/core/platform/cpu_feature_guard.cc:142] Your CPU supports instructions that this TensorFlow binary was not compiled to use: AVX2 FMA

Advanced Vector Extensions (AVX) are extensions to the x86 instruction set architecture for microprocessors from Intel and AMD proposed by Intel in March 2008 and first supported by Intel with the Sandy Bridge processor shipping in Q1 2011 and later on by AMD with the Bulldozer processor shipping in Q3 2011. AVX provides new features, new instructions, and a new coding scheme.

AVX introduces fused multiply-accumulate (FMA) operations, which speed up linear algebra computation, namely dot-product, matrix multiply, convolution, etc. Almost every machine-learning training involves a great deal of these operations, hence will be faster on a CPU that supports AVX and FMA (up to 300%).

We won’t ignore the warning message and we will compile TF from source.

We will start with uninstalling the default version of Tensorflow:

The bazel build command creates an executable named build_pip_package—this is the program that builds the pip package. Run the executable as shown below to build a .whl package in the /tmp/tensorflow_pkg directory.

Airflow was started in October 2014 by Maxime Beauchemin at Airbnb. It was open source from the very first commit and officially brought under the Airbnb GitHub and announced in June 2015.

The project joined the Apache Software Foundation’s Incubator program in March 2016 and the Foundation announced Apache Airflow as a Top-Level Project in January 2019.

Apache Airflow is in use at more than 200 organizations, including Adobe, Airbnb, Astronomer, Etsy, Google, ING, Lyft, NYC City Planning, Paypal, Polidea, Qubole, Quizlet, Reddit, Reply, Solita, Square, Twitter, and United Airlines, among others.

Introduction

Airflow is a platform to programmatically author, schedule and monitor workflows.

Use airflow to author workflows as directed acyclic graphs (DAGs) of tasks. The airflow scheduler executes your tasks on an array of workers while following the specified dependencies. Rich command line utilities make performing complex surgeries on DAGs a snap. The rich user interface makes it easy to visualize pipelines running in production, monitor progress, and troubleshoot issues when needed.

When workflows are defined as code, they become more maintainable, versionable, testable, and collaborative.

Workflows

We’ll create a workflow by specifying actions as a Directed Acyclic Graph (DAG) in Python. The tasks of a workflow make up a Graph; the graph is Directed because the tasks are ordered; and we don’t want to get stuck in an eternal loop so the graph also has to be Acyclic.

The figure below shows an example of a DAG:

Installation

pip3 install apache-airflow

airflow version

AIRFLOW_HOME is the directory where you store your DAG definition files and Airflow plugins

mkdir Airflow

export AIRFLOW_HOME=`pwd`/Airflow

Airflow requires a database to be initiated before you can run tasks. If you’re just experimenting and learning Airflow, you can stick with the default SQLite option.

airflow initdb

ls -l Airflow/

The database airflow.db is created

You can start Airflow UI by issuing the following command:

We’ll start by creating a Hello World workflow, which does nothing other then sending “Hello world!” to the log.

Create your dags folder, that is the directory where your DAG definition files will be stored in AIRFLOW_HOME/dags. Inside that directory create a file named hello_world.py:

mkdir dags

Add the following code to dags/hello_world.py

from datetime import datetime

from airflow import DAG

from airflow.operators.dummy_operator import DummyOperator

from airflow.operators.python_operator import PythonOperator

def print_hello():

return 'Hello world!'

dag = DAG('hello_world', description='Simple tutorial DAG',

schedule_interval='0 12 * * *',

start_date=datetime(2019, 5, 29), catchup=False)

dummy_operator = DummyOperator(task_id='dummy_task', retries=3, dag=dag)

hello_operator = PythonOperator(task_id='hello_task', python_callable=print_hello, dag=dag)

dummy_operator >> hello_operator

This file creates a simple DAG with just two operators, the DummyOperator, which does nothing and a PythonOperator which calls the print_hello function when its task is executed.

Running your DAG

Open a second terminal, go to the AIRFLOW_HOME folder and start the Airflow scheduler by issuing :

export AIRFLOW_HOME=`pwd`

airflow scheduler

When you reload the Airflow UI in your browser, you should see your hello_world DAG listed in Airflow UI.

In order to start a DAG Run, first turn the workflow on, then click the Trigger Dag button and finally, click on the Graph View to see the progress of the run.

After clicking the Graph View:

You can reload the graph view until both tasks reach the status Success.

When they are done, you can click on the hello_task and then click View Log.

If everything worked as expected, the log should show a number of lines and among them something like this:

Your first Airflow Operator

Let’s start writing our own Airflow operators. An Operator is an atomic block of workflow logic, which performs a single action. Operators are written as Python classes (subclasses of BaseOperator), where the __init__ function can be used to configure settings for the task and a method named execute is called when the task instance is executed.

Any value that the execute method returns is saved as an Xcom message under the key return_value. We’ll cover this topic later.

The execute method may also raise the AirflowSkipException from airflow.exceptions. In such a case the task instance would transition to the Skipped status.

If another exception is raised, the task will be retried until the maximum number of retries is reached.

Remember that since the execute method can retry many times, it should be idempotent [it can be applied multiple times without changing the result beyond the initial application]

We’ll create your first operator in an Airflow plugin file named plugins/my_operators.py. First create the /plugins directory, then add the my_operators.py file with the following content:

import logging

from airflow.models import BaseOperator

from airflow.plugins_manager import AirflowPlugin

from airflow.utils.decorators import apply_defaults

log = logging.getLogger(__name__)

class MyFirstOperator(BaseOperator):

@apply_defaults

def __init__(self, my_operator_param, *args, **kwargs):

self.operator_param = my_operator_param

super(MyFirstOperator, self).__init__(*args, **kwargs)

def execute(self, context):

log.info("Hello World!")

log.info('operator_param: %s', self.operator_param)

class MyFirstPlugin(AirflowPlugin):

name = "my_first_plugin"

operators = [MyFirstOperator]

In this file we are defining a new operator named MyFirstOperator. Its execute method is very simple, all it does is log “Hello World!” and the value of its own single parameter. The parameter is set in the __init__ function.

We are also defining an Airflow plugin named MyFirstPlugin. By defining a plugin in a file stored in the /plugins directory, we’re providing Airflow the ability to pick up our plugin and all the operators it defines. We’ll be able to import these operators later using the line from airflow.operators import MyFirstOperator.

Now, we’ll need to create a new DAG to test our operator. Create a dags/test_operators.py file and fill it with the following content:

from datetime import datetime

from airflow import DAG

from airflow.operators.dummy_operator import DummyOperator

from airflow.operators import MyFirstOperator

dag = DAG('my_test_dag', description='Another tutorial DAG',

schedule_interval='0 12 * * *',

start_date=datetime(2019, 5, 29), catchup=False)

dummy_task = DummyOperator(task_id='dummy_task', dag=dag)

operator_task = MyFirstOperator(my_operator_param='This is a test.',

task_id='my_first_operator_task', dag=dag)

dummy_task >> operator_task

Here we just created a simple DAG named my_test_dag with a DummyOperator task and another task using our new MyFirstOperator. Notice how we pass the configuration value for my_operator_param here during DAG definition.

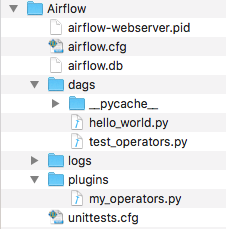

At this stage your source tree looks like this:

To test your new operator, you should stop (CTRL-C) and restart your Airflow web server and scheduler. Afterwards, go back to the Airflow UI, turn on the my_test_dag DAG and trigger a run. Take a look at the logs for my_first_operator_task.

Your first Airflow Sensor

An Airflow Sensor is a special type of Operator, typically used to monitor a long running task on another system.

To create a Sensor, we define a subclass of BaseSensorOperator and override its poke function. The poke function will be called over and over every poke_interval seconds until one of the following happens:

poke returns True – if it returns False it will be called again.

poke raises an AirflowSkipException from airflow.exceptions – the Sensor task instance’s status will be set to Skipped.

poke raises another exception, in which case it will be retried until the maximum number of retries is reached.

As an example, SqlSensor runs a sql statement until a criteria is met, HdfsSensor waits for a file or folder to land in HDFS, S3KeySensor waits for a key (a file-like instance on S3) to be present in a S3 bucket), S3PrefixSensor waits for a prefix to exist and HttpSensor executes a HTTP get statement and returns False on failure.

To add a new Sensor to your my_operators.py file, add the following code:

from datetime import datetime

from airflow.operators.sensors import BaseSensorOperator

class MyFirstSensor(BaseSensorOperator):

@apply_defaults

def __init__(self, *args, **kwargs):

super(MyFirstSensor, self).__init__(*args, **kwargs)

def poke(self, context):

current_minute = datetime.now().minute

if current_minute % 3 != 0:

log.info("Current minute (%s) not is divisible by 3, sensor will retry.", current_minute)

return False

log.info("Current minute (%s) is divisible by 3, sensor finishing.", current_minute)

return True

Here we created a very simple sensor, which will wait until the the current minute is a number divisible by 3. When this happens, the sensor’s condition will be satisfied and it will exit. This is a contrived example, in a real case you would probably check something more unpredictable than just the time.

Remember to also change the plugin class, to add the new sensor to the operators it exports:

class MyFirstPlugin(AirflowPlugin):

name = "my_first_plugin"

operators = [MyFirstOperator, MyFirstSensor]

The final my_operators.py file is:

import logging

from airflow.models import BaseOperator

from airflow.plugins_manager import AirflowPlugin

from airflow.utils.decorators import apply_defaults

from datetime import datetime

from airflow.operators.sensors import BaseSensorOperator

log = logging.getLogger(__name__)

class MyFirstOperator(BaseOperator):

@apply_defaults

def __init__(self, my_operator_param, *args, **kwargs):

self.operator_param = my_operator_param

super(MyFirstOperator, self).__init__(*args, **kwargs)

def execute(self, context):

log.info("Hello World!")

log.info('operator_param: %s', self.operator_param)

class MyFirstSensor(BaseSensorOperator):

@apply_defaults

def __init__(self, *args, **kwargs):

super(MyFirstSensor, self).__init__(*args, **kwargs)

def poke(self, context):

current_minute = datetime.now().minute

if current_minute % 3 != 0:

log.info("Current minute (%s) not is divisible by 3, sensor will retry.", current_minute)

return False

log.info("Current minute (%s) is divisible by 3, sensor finishing.", current_minute)

return True

class MyFirstPlugin(AirflowPlugin):

name = "my_first_plugin"

operators = [MyFirstOperator, MyFirstSensor]

You can now place the operator in your DAG, so the new test_operators.py file looks like:

from datetime import datetime

from airflow import DAG

from airflow.operators.dummy_operator import DummyOperator

from airflow.operators import MyFirstOperator, MyFirstSensor

dag = DAG('my_test_dag', description='Another tutorial DAG',

schedule_interval='0 12 * * *',

start_date=datetime(2019, 5, 29), catchup=False)

dummy_task = DummyOperator(task_id='dummy_task', dag=dag)

sensor_task = MyFirstSensor(task_id='my_sensor_task', poke_interval=30, dag=dag)

operator_task = MyFirstOperator(my_operator_param='This is a test.',

task_id='my_first_operator_task', dag=dag)

dummy_task >> sensor_task >> operator_task

Restart your webserver and scheduler and try out your new workflow. The Graph View looks like:

If you click View log of the my_sensor_task task, you should see something similar to this:

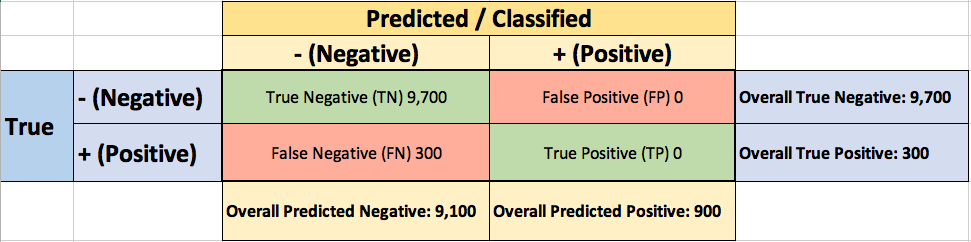

Your boss asked you to build a fraud detection classifier, so you’ve created one.

The output of your fraud detection model is the probability [0.0-1.0] that a transaction is fraudulent. If this probability is below 0.5, you classify the transaction as non-fraudulent; otherwise, you classify the transaction as fraudulent.

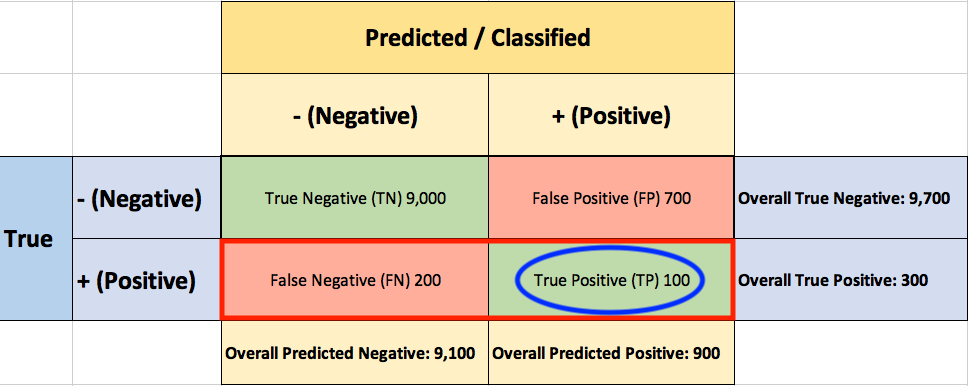

To evaluate the performance of your model, you collect 10,000 manually classified transactions, with 300fraudulent transaction and 9,700non-fraudulent transactions. You run your classifier on every transaction, predict the class label (fraudulent or non-fraudulent) and summarise the results in the following confusion matrix:

A True Positive(TP=100) is an outcome where the model correctly predicts the positive(fraudulent) class. Similarly, a True Negative(TN=9,000) is an outcome where the model correctly predicts the negative(non-fraudulent) class.

A False Positive(FP=700) is an outcome where the model incorrectly predicts the positive(fraudulent) class. And a False Negative(FN=200) is an outcome where the model incorrectly predicts the negative(non-fraudulent) class.

Asking yourself what percent of your predictions were correct, you calculate the accuracy:

Wow, 91% accuracy! Just before sharing the great news with your boss, you notice that out of the 300 fraudulent transactions, only 100 fraudulent transactions are classified correctly. Your classifier missed 200 out of the 300 fraudulent transactions!

Your colleague, hardly hiding her simile, suggests a “better” classifier. Her classifier predicts every transaction as non-fraudulent (negative), with a staggering 97% accuracy!

While 97%accuracy may seem excellent at first glance, you’ve soon realized the catch: your boss asked you to build a fraud detection classifier, and with the always-return-non-fraudulent classifier you will miss all the fraudulent transactions.

“Nothing travels faster than the speed of light, with the possible exception of bad news, which obeys its own special laws.”

Douglas Adams

You learned the hard-way that accuracy can be misleading and that for problems like this, additional measures are required to evaluate your classifier.

You start by asking yourself what percent of the positive (fraudulent) cases did you catch? You go back to the confusion matrix and divide the True Positive (TP – blue oval) by the overall number of true fraudulent transactions (red rectangle)

So the classier caught 33.3% of the fraudulent transactions.

Next, you ask yourself what percent of positive (fraudulent) predictions were correct? You go back to the confusion matrix and divide the True Positive (TP – blue oval) by the overall number of predicted fraudulent transactions (red rectangle)

So now you know that when your classifier predicts that a transaction is fraudulent, only 12.5% of the time your classifier is correct.

F1 Score combines Recall and Precision to one performance metric. F1 Score is the weighted average of Precision and Recall. Therefore, this score takes both false positives and false negatives into account. F1 is usually more useful than Accuracy, especially if you have an uneven class distribution.

Finally, you ask yourself what percent of negative (non-fraudulent) predictions were incorrect? You go back to the confusion matrix and divide the False Positive (FP – blue oval) by the overall number of truenon-fraudulent transactions (red rectangle)

7.2% of the non-fraudulent transactions were classifiedincorrectly as fraudulent transactions.

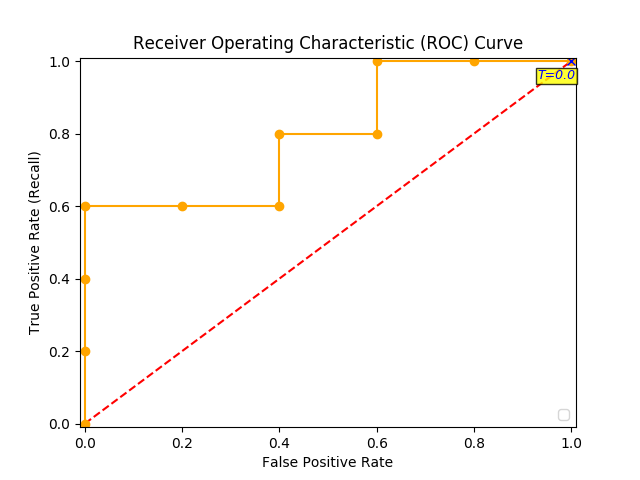

ROC (Receiver Operating Characteristics)

You soon learn that you must examine both Precision and Recall. Unfortunately, Precision and Recall are often in tension. That is, improving Precision typically reduces Recall and vice versa.

The overall performance of a classifier, summarized over all possible thresholds, is given by the Receiver Operating Characteristics (ROC) curve. The name “ROC” is historical and comes from communications theory. ROC Curves are used to see how well your classifier can separate positive and negative examples and to identify the best threshold for separating them.

To be able to use the ROC curve, your classifier should be able to rank examples such that the ones with higher rank are more likely to be positive (fraudulent). As an example, Logistic Regression outputs probabilities, which is a score that you can use for ranking.

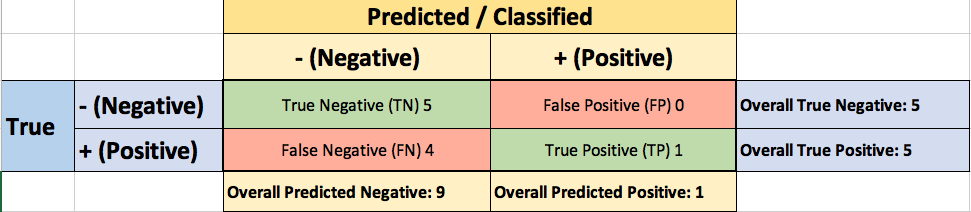

You train a new model and you use it to predict the outcome of 10 new test transactions, summarizing the result in the following table: the values of the middle column (True Label) are either zero (0) for non-fraudulent transactions or one (1) for fraudulent transactions, and the last column (Fraudulent Prob) is the probability that the transaction is fraudulent:

Remember the 0.5 threshold? If you are concerned about missing the two fraudulent transactions (red circles), then you may consider lowering this threshold.

For instance, you might lower the threshold and label any transaction with a probability below 0.1 to the non-fraudulent class, catching the two fraudulent transactions that you previously missed.

To derive the ROC curve, you calculate the True Positive Rate (TPR) and the False Positive Rate (FPR), starting by setting the threshold to 1.0, where every transaction with a Fraudulent Prob of less than 1.0 is classified as non-fraudulent (0). The column “T=1.0” shows the predicted class labels when the threshold is 1.0:

The confusion matrix for the Threshold=1.0 case:

The ROC curve is created by plotting the True Positive Pate (TPR) against the False Positive Rate (FPR) at various threshold settings, so you calculate both:

You summarize it in the following table:

Now you can finally plot the first point on your ROC graph! A random guess would give a point along the dotted diagonal line (the so-called line of no-discrimination) from the left bottom to the top right corners

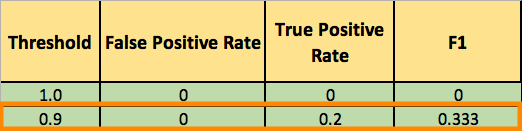

You now lower the threshold to 0.9, and recalculate the FPR and the TPR:

The confusion matrix for Threshold=0.9:

Adding a new row to your summary table:

You continue and plot the True Positive Pate (TPR) against the False Positive Rate (FPR) at various threshold settings:

Receiver Operating Characteristics (ROC) curve

And voila, here is your ROC curve!

AUC (Area Under the Curve)

The model performance is determined by looking at the area under the ROC curve (or AUC). An excellent model has AUC near to the 1.0, which means it has a good measure of separability. For your model, the AUC is the combined are of the blue, green and purple rectangles, so the AUC = 0.4 x 0.6 + 0.2 x 0.8 + 0.4 x 1.0 = 0.80.

You can validate this result by calling roc_auc_score, and the result is indeed 0.80.

Conclusion

Accuracy will not always be the metric.

Precision and recall are often in tension. That is, improving precision typically reduces recall and vice versa.

AUC-ROC curve is one of the most commonly used metrics to evaluate the performance of machine learning algorithms.

ROC Curves summarize the trade-off between the true positive rate and false positive rate for a predictive model using different probability thresholds.

The ROC curve can be used to choose the best operating point.

Thanks for Reading! You can reach me at LinkedIn and Twitter.

References:

[1] An Introduction to Statistical Learning [James, Witten, Hastie, and Tibshirani]

Make sure you have Java 8 or higher installed on your computer and visit the Spark download page

Select the latest Spark release, a prebuilt package for Hadoop, and download it directly.

Unzip it and move it to your /opt folder:

$ tar -xzf spark-2.4.0-bin-hadoop2.7.tgz $ sudo mv spark-2.4.0-bin-hadoop2.7 /opt/spark-2.4.0

A symbolic link is like a shortcut from one file to another. The contents of a symbolic link are the address of the actual file or folder that is being linked to.

Create a symbolic link (this will let you have multiple spark versions):

Finally, tell your bash where to find Spark. To find what shell you are using, type:

$ echo $SHELL /bin/bash

To do so, edit your bash file:

$ nano ~/.bash_profile

configure your $PATH variables by adding the following lines to your ~/.bash_profile file:

export SPARK_HOME=/opt/spark export PATH=$SPARK_HOME/bin:$PATH # For python 3, You have to add the line below or you will get an error export PYSPARK_PYTHON=python3

Now to run PySpark in Jupyter you’ll need to update the PySpark driver environment variables. Just add these lines to your ~/.bash_profile file:

Restart (our just source) your terminal and launch PySpark:

$ pyspark

This command should start a Jupyter Notebook in your web browser. Create a new notebook by clicking on ‘New’ > ‘Notebooks Python [default]’.

Running PySpark in Jupyter Notebook

The PySpark context can be

sc = SparkContext.getOrCreate()

To check if your notebook is initialized with SparkContext, you could try the following codes in your notebook:

sc = SparkContext.getOrCreate()

import numpy as np

TOTAL = 10000

dots = sc.parallelize([2.0 * np.random.random(2) - 1.0 for i in range(TOTAL)]).cache()

print("Number of random points:", dots.count())

stats = dots.stats()

print('Mean:', stats.mean())

print('stdev:', stats.stdev())

The result:

Running PySpark in your favorite IDE

Sometimes you need a full IDE to create more complex code, and PySpark isn’t on sys.path by default, but that doesn’t mean it can’t be used as a regular library. You can address this by adding PySpark to sys.path at runtime. The package findspark does that for you.

To install findspark just type:

$ pip3 install findspark

And then on your IDE (I use Eclipse and Pydev) to initialize PySpark, just call:

Interesting presentation today at the DataScience SG meet-up

Conventional

fraud prevention methods are rule based, expansive and slow to implement

Q1 2016: $5

of every $100 subject to fraud attack!

Key fraud types: account takeover, friendly fraud & fraud due to stolen card information

Consumers want: easy, instant, customized, mobile and dynamic options to suit their personal situation. Consumers do NOT want to be part of the fraud detection process.

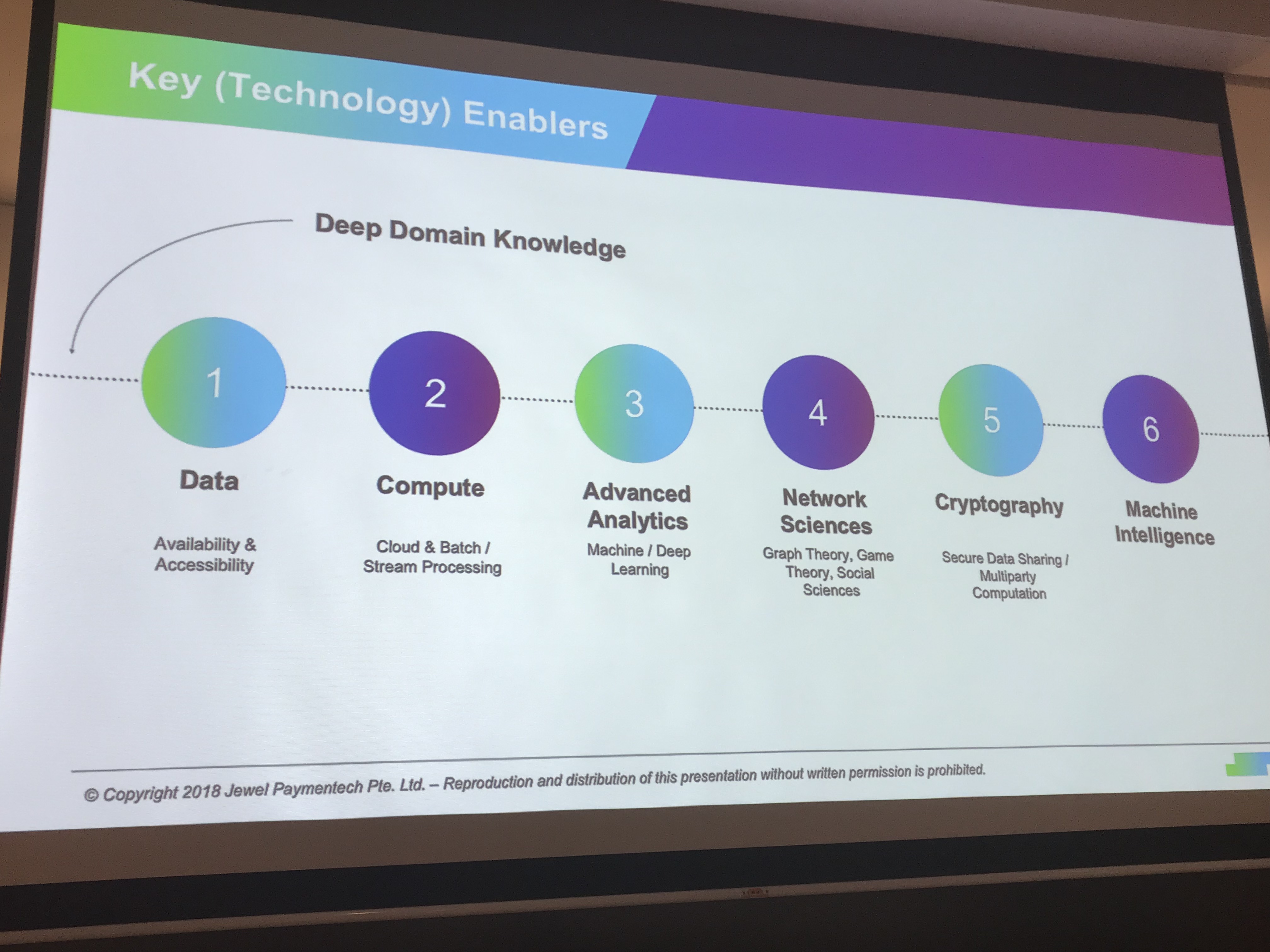

Key technology enablers:

Historically fraud detection systems have relied on rues hand-curated by fraud experts to catch fraudulent activity.

An auto-encoder is a neural network trained to reconstruct its inputs, which forces a hidden layer to try and to learn good representations of the input

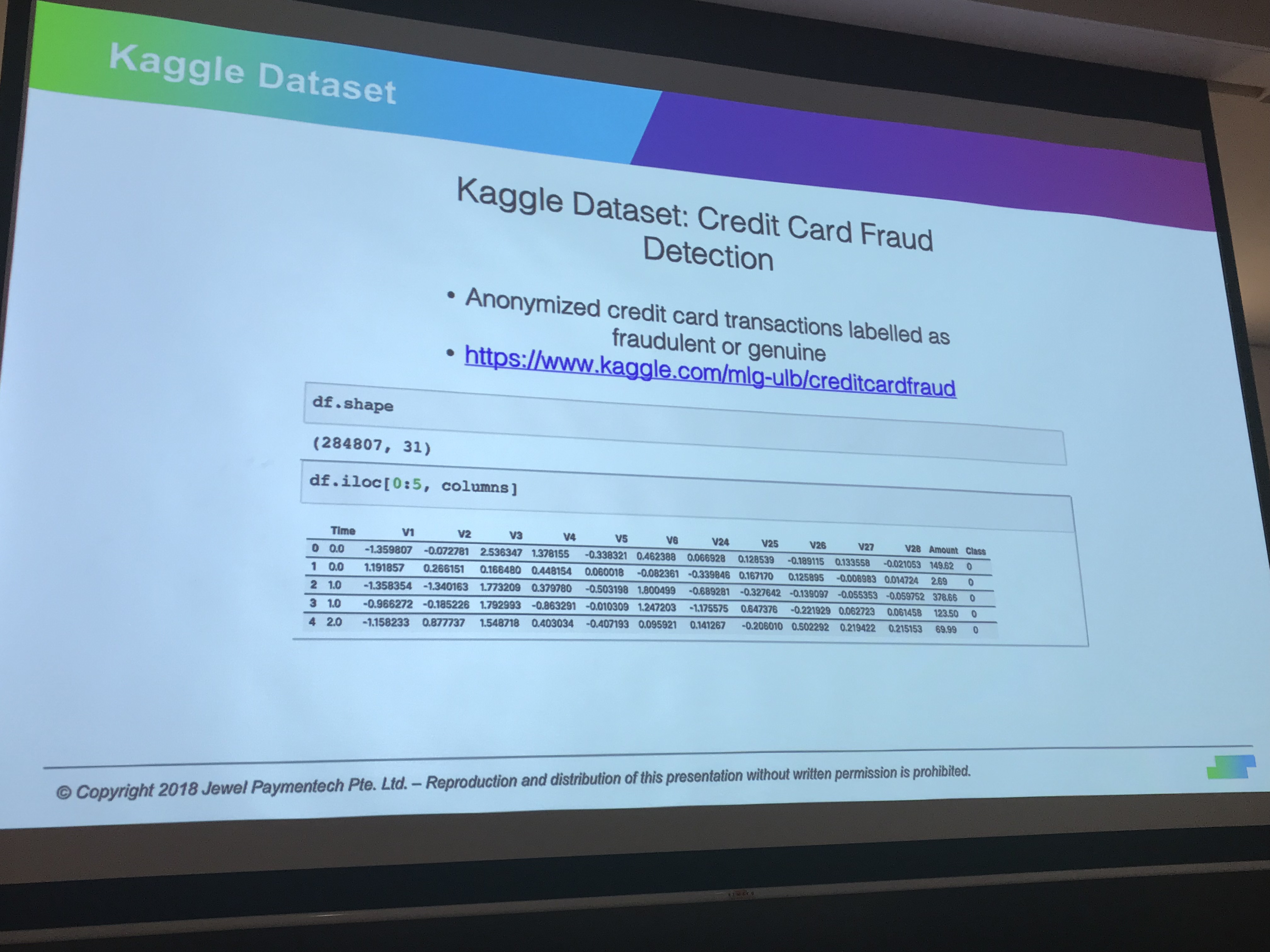

Kaggle dataset:

Train Autoencoder on normal transactions and using the Autoencoder transformation there is now a clear separation between the normal and the fraudulent transactions.

The December PyData Meetup started with Luis Smith, Data Scientist at GO-JEK, sharing the Secret Recipe Behind GO-FOOD’s Recommendations:

“For GO-FOOD, we believe the key to unlocking good recommendations is to derive vector representations for our users, dishes, and merchants. This way we are able to capture our users’ food preferences and recommend them the most relevant merchants and dishes.”

How do people think about the food?

Flavor profile

Trendy

Value for money

Portion size

Ingredients

… and much more

The preferred approach is to let the transactional data discover the pattern.

A sample ETL workflow:

Using StarSpace to learn the vector representations:

Go-Jek formulation of the problem:

User-to-dish similarity is surfaced in the app via the “dishes you might like”. The average vector of customer’s purchases represents the recommended dish.

Due to data sparsity, item-based collaborative filtering is used for merchant recommendation.

The cold start problem is still an issue, for inactive users or users that purchase infrequently.

What a great symposium! Thank you Dr. Linlin Li, Prof. Ido Dagan, Prof. Noah Smith and the rest of the speakers for the interesting talks and thank you Singapore University of Technology and Design (SUTD) for hosting this event. Here is a quick summary of the first half of the symposium, you can learn more by looking for the papers published by these research groups:

Linlin Li: The text processing engine that powers Alibaba’s business applications

Dr. Linlin Li from Alibaba presented the mission of Alibaba’s NLP group and spoke about AliNLP, a large scale NLP technology platform for the entire Alibaba Eco-system, dealing with data collection and multilingual algorithms for lexical, syntactic, semantic, discourse analysis and distributed representation of text.

Alibaba is also helping to improve the quality of the Electronic Medical Records (EMRs) in China, traditionally done by labour intensive methods.

Ido Dagan: Consolidating Textual Information

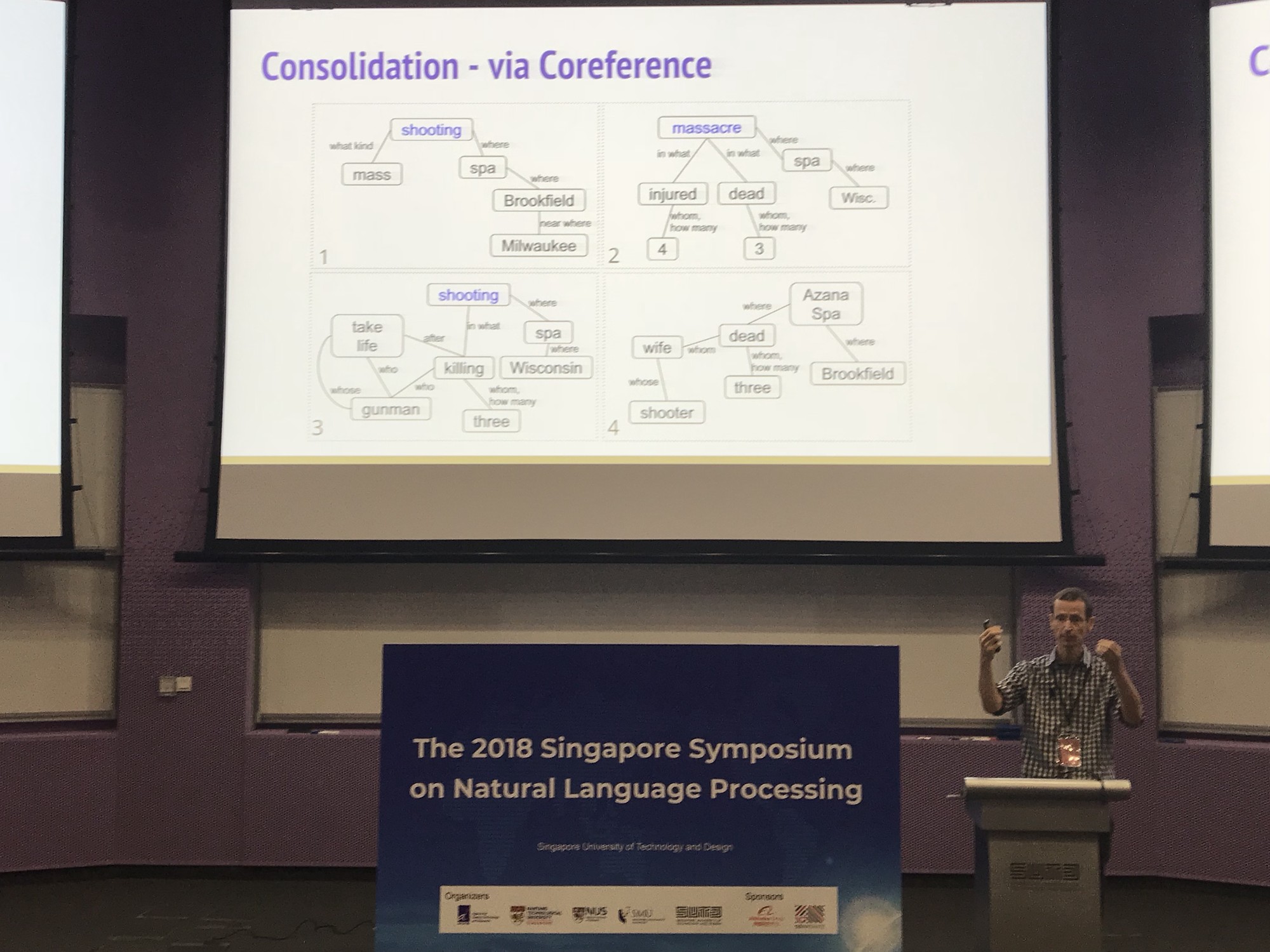

Prof. Ido Dagan gave an excellent presentation on Natural Knowledge Consolidating Textual Information. Texts come in large multitudes, such as news story, search results, and product reviews. Search interfaces hasn’t changed much in decades, which make them accessible, but hard to consume. For example, the news tweets illustration in the slide below shows that here is a lot of redundancy and complementary information, so there is a need to consolidate the knowledge within multiple texts.

Generic knowledge representation via structured knowledge graphs and semantic representation are often being used, where both approaches require an expert to annotate the dataset, which is expansive and hard to replicate.

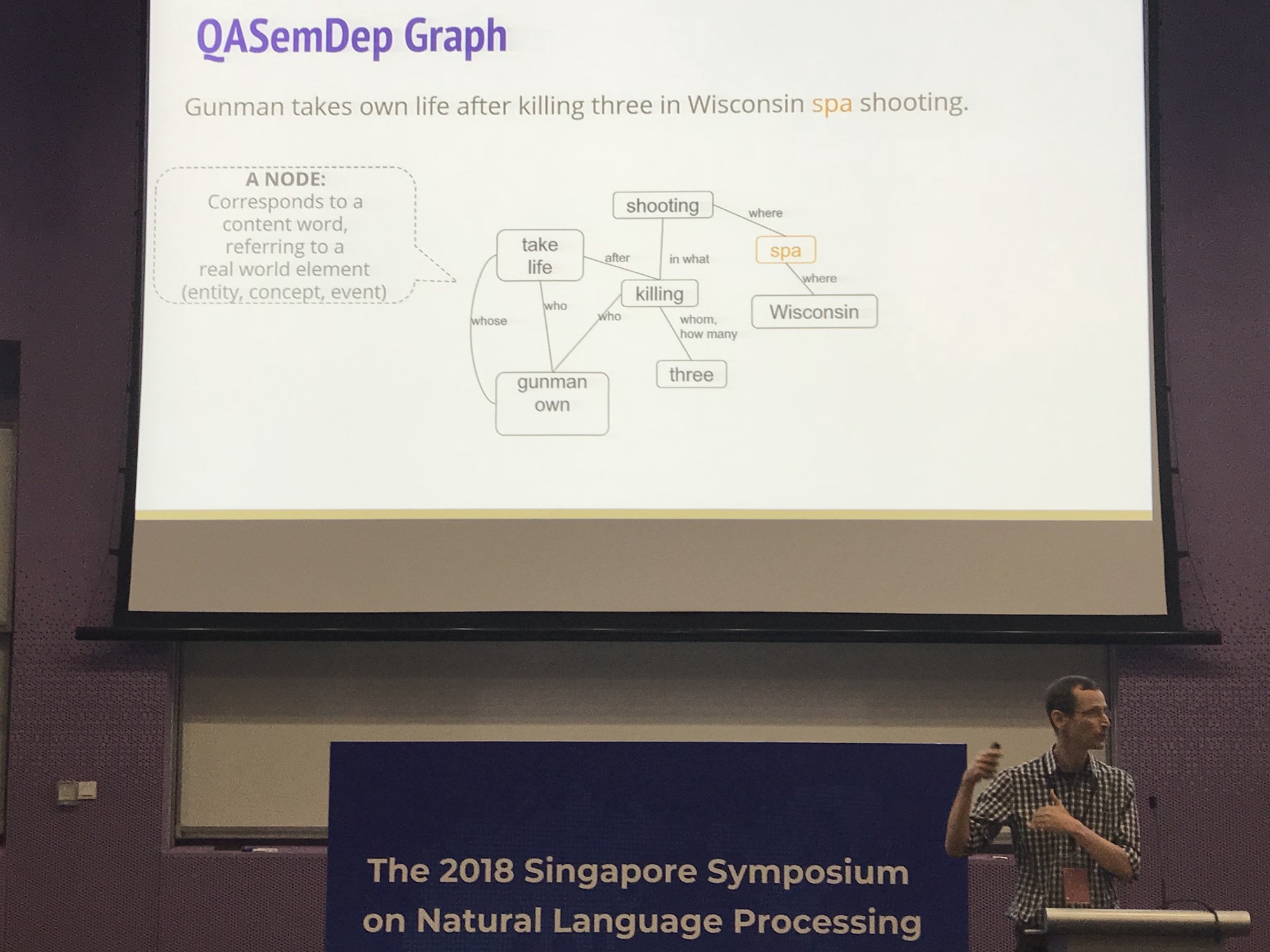

The structure of a single sentence will look like this:

The information can be consolidated across the various data sources via Coreference

To conclude

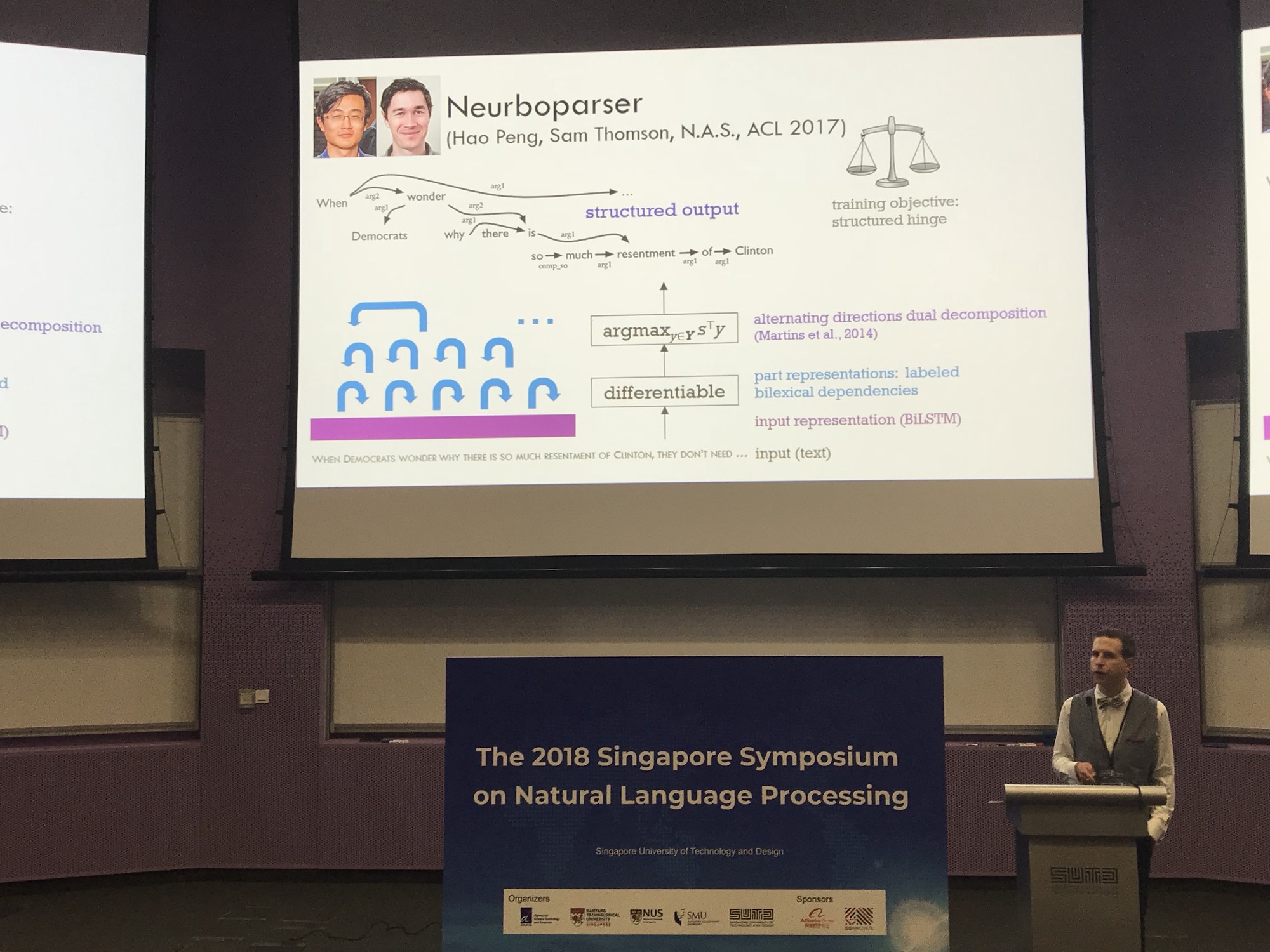

Noah A. Smith: Syncretizing Structured and Learned Representation

Prof. Noah described new ways to use representation learning for NLP

Some promising results

Prof. Noah presented different approaches to solve backpropagation with structure in the middle, where the intermediate representation is non-differentiable.